Most Americans have a faulty strategic vision. Instead of seeing the three primary strategic colors, they only perceive two of them: premium and cost leadership. Differentiation is mistaken with premium and low cost is confused with cost-volume leadership.

There is a general consensus to consider that there are two generic strategies: differentiation and cost-volume leadership. Yet most Americans perceive only one side of differentiation and mistake the other side with cost-volume leadership. Differentiation is often equated with its upward form: premium; and its downward form, low-cost, is usually confused with cost-volume. The distinction between the two strategies is however easy to make. A cost-volume strategy provides the benchmark offer at a lower price (eg. Walmart), whereas a low cost strategy produces a degraded version of the benchmark offer, stripped of all dispensable features (eg. Aldi).

Contemplating differentiation, the low cost option is generally disregarded in comparison to the premium alternative. Most managers have a premium bias and an irrepressible tendency to offer additional value to clients. Trading up is the quasi-systematic answer to the well-known “commodity trap”: more quality, more functionalities, more customer intimacy, more related services, more ergonomics, more flattering branding, better customer experiences, more integrated solutions…., even though a large number of customers are not willing to pay for it.

Many companies fight this faltering willingness to pay by boosting their sales & marketing efforts and strengthening their innovation department. They exhaust themselves trying to justify the price difference and educating their customers. This noble endeavor is bound to fail with clients who just want to have their basic needs satisfied. Low cost business models go against this trend for ever more sophistication, convenience and speed. They attract many consumers who accept less comfort and less ego-massaging in exchange for drastic price reductions.

The magic of the downward form of differentiation

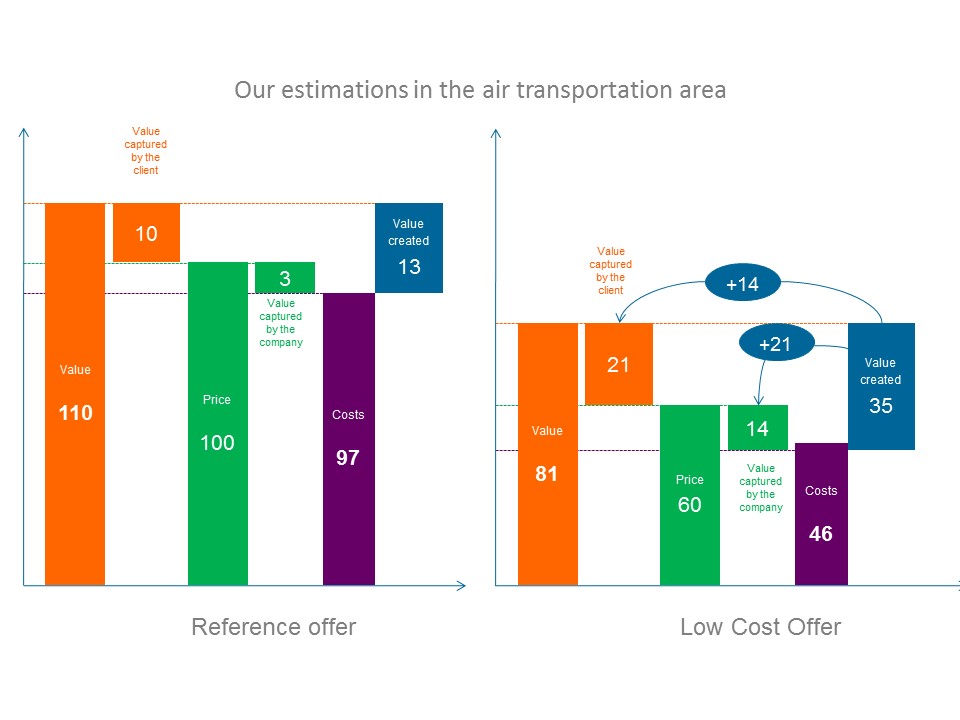

For differentiation to be viable, whether upward or downward, the following “golden rule” has to be respected. The rationale behind this “golden rule” is that if you want to divert customers from the mainstream offer, the increase in value has to be superior to the price increment; otherwise they would have no interest in switching to premium. Likewise, to attract clients in the case of low cost, the decrease in value, measured in absolute terms, has to be inferior to the decrease in price. Then, if you don’t want to compromise your profitability, costs have to vary less than prices in the case of premium and more than prices in the case of low-cost.

| Differentiation Golden Rule

∆ Value > ∆ Price > ∆ Costs where ∆ is the difference between the differentiated offer and the reference (mainstream) Offer Ex : upward differentiation (premium): +50 > + 30> +20 Ex : downward differentiation (low cost): – 20> -45 > -55 |

The paradox is that low prices for clients in a low-cost business model, doesn’t imply low profitability for companies. That’s why low-cost strategies make up an unorthodox win-win model. Customers do give up part of the value that comes with the reference offer but the sacrifice they make is largely offset by the money they save. On the other hand, bottom lines are not penalized by the low prices, as the streamlined value proposition and architecture are driving the costs down, and even further than the price reduction. Our research shows that low cost strategies that comply with the golden rule are creating more value for their clients and themselves than benchmark offers. The short-haul airline industry provides a good illustration of the phenomenon (Fig.1).

Fig 1: the example of the short-haul airline industry

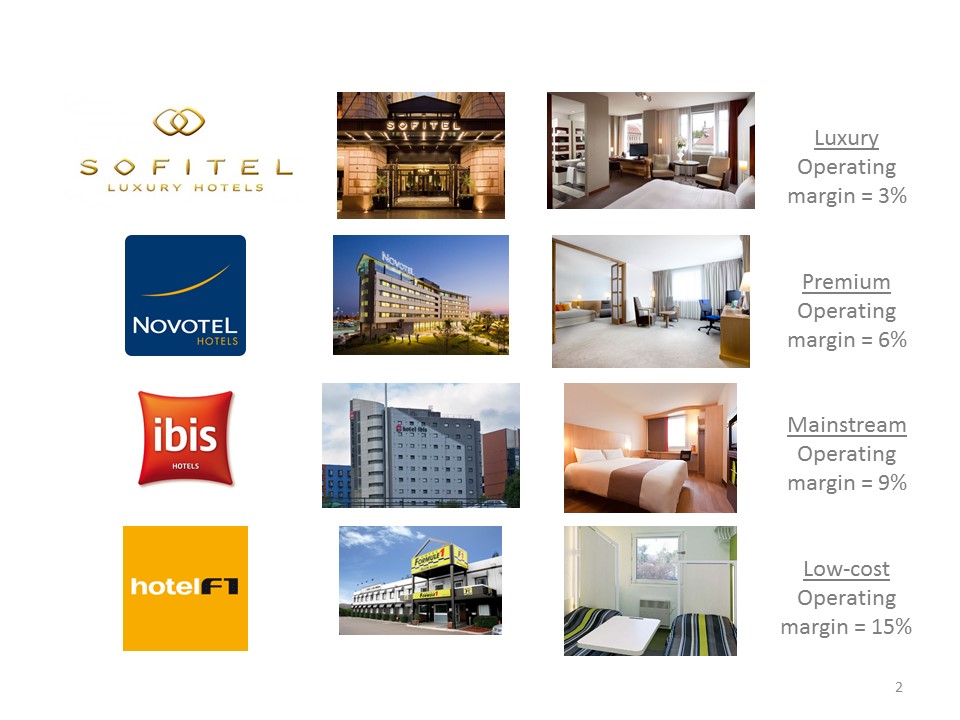

The financials of low-cost players are upgraded (see fig. 2 for an overview of the average profitability of the different business models run by the Accor Group in the hotel industry, or table 1 for financials in the airline industry). It comes not only from the lower cost base, but also from the additional revenues and the improved assets turnover. Clients are attracted by very cheap prices but are pushed to buy additional features, services or goods. It will cost you only 29 $ to fly from New York to Florida but you will have to add 35$ for a pre-booked hand luggage. Ancillary revenues make up 40% of the sales of Spirit Airlines and 25% of the European leader Ryan Air. Low-cost financials are also characterized by an enhanced assets turnover, which combined with less assets requirements, results in a better return on capital employed. Occupancy rates are indeed higher in low-cost hotels (80% vs 65%) or car rentals (70% vs 60%); number of daily rotations per plane is higher (planes fly 11 hours a day vs 8 hours), sales per square meter are higher in hard-discount retail….

| Company | Operating margin | Return on capital

Employed |

| Low Cost : South West Airlines | 21% | 10% |

| Low Cost : Ryan Air | 22% | 14% |

| Lufthansa | 5% | 4% |

| Air France-KLM | 5% | 2% |

Table1: 2015 Financials of low-cost operators vs legacy companies (Source Reuters)

Fig. 2: Windfall profits from the low-cost segment. Standard profitability of the different business models run by the Accor Group in the hotel industry

Fig. 2: Windfall profits from the low-cost segment. Standard profitability of the different business models run by the Accor Group in the hotel industry

How to design a low-cost business model

Becoming low cost involves the restructuring the value architecture, which can be achieved through several routes. The first route is the self-limitation that comes directly from the purification and simplification of the value proposition. The offering is not only simpler but entails less comfort for the client, which enables the removal of entire steps in the value chain, such as distribution through retail outlets or intermediaries, customer support, various customer services (even basic ones like exchange or refund), design and implementation of nice displays, marketing and sales effort (the price speaks for itself and is disseminated via journalists and word-of-mouth). The offer is a “take it or leave it” offer. So no adjustment, variation or customization of the core offer is available.

The second route derives from this extreme standardization and entails massive volume effects. In a self-perpetuating virtuous circle, the low prices attract customers, which in turn intensify the scale effects. The third lever is the transfer to clients or to automated systems of some of the tasks usually carried out by employees in the company. This may take the form of administrative tasks (booking, payment, printing), customer service which becomes self-help, additional transportation efforts borne by the clients, co-production of the service (like clients washing their own hair). Finally, the fourth level of cost reduction is the higher productivity of the workforce, whether they are less paid, more versatile, putting in more hours or more autonomous with less management.

Low cost offerings create so much customer and financial value that its path can no longer be overlooked by companies aspiring to reinvent themselves.

| SUMMARY: What is a low cost business model?

Value proposition A simple offering, streamlined of any superfluous attributes, focused on meeting basic needs Prices which stand out from competition A lower level of comfort for clients, who have to sacrifice convenience, but paradoxically nice surprises on certain dimensions (processing speed, robustness,…) Value architecture Self-limitation : removal of some costly steps in the value chain (a direct consequence of the elimination of value attributes), stark reduction in variety and complexity, no customization, refusal to handle special cases or to address certain groups of “privileged“ customers, limited innovation, re-use of pre-existing components, Scale effects. Automation & co-production by the customer More productive, more versatile and autonomous staff Value equation Improved profitability: the dramatic cost reduction is not fully passed on to customers Development of ancillary revenues. Some of the frills of the reference offer are proposed as a chargeable option. Less investment, better assets turnover. Hence better return on capital employed |