One pillar of the traditional strategic thinking is falling apart. Decision-makers who still adhere to the old paradigm will be losing valuable growth opportunities.

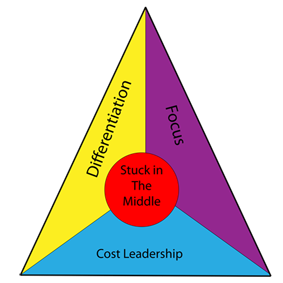

Since Porter’s seminal work in the 80’s, firms are supposed to choose sides: either differentiation or cost leadership. If they fail to do, they may fall into the trap of being “stuck in the middle” with no clear competitive advantage. Companies trying to combine the two generic strategies are expected to underperform their focused peers for three reasons. First, being average on several value dimensions, they won’t attract clients. Secondly, they will suffer from higher costs because of the inconsistency of their value chain. Finally, their lack of strategic clarity will result in internal confusion and excessive complexity.

That counter-examples exist is not a new insight. Samsung semiconductors, Ikea, Zara…, are the living proof that firms can enjoy a dual competitive advantage and reconcile differentiation and cost. Nevertheless these cases have not invalidated the general belief that firms belong to mutually exclusive strategic groups. Firms may deviate from the core strategic pattern of their group, but within the limits of their initial choice (cost leadership or differentiation). For instance, Zara may give more value for money than Gap, but cannot vie with Gucci or Prada.

We have however reached a moment where exceptions have accumulated to the point that they are questioning the relevance and the simplicity of Porter’s framework. In many industries, major players are having it both ways and are running supposedly incompatible business models. It used to be impossible to be present at both ends of the market and disprove the fate of one’s initial positioning. Stelios Haji-Ioannou, the founder of easyJet used to claim vigorously: “You don’t become low-cost, you are born low-cost.” His assertion was based on the failures of many airlines in the 90’s and early 2000s that had tried to become low-cost (Delta with Song, United with Ted, British Airways with Go Fly, KLM with Buzz, SAS with Snowflake). But what may have been true 15 years ago is no longer valid. The world reference for premium service Singapore Airlines has thriving Low Cost branches with Scoot and Tiger Air.

Many pioneering companies are nowadays simultaneously pursuing cost and differentiation, sometimes without the clients’ knowledge, thanks to a multiple branding. Hybrid value chains have emerged, with activities being shared and others being redundant or specific. Far from creating inefficiencies in terms of unnecessary costs or insufficient value, these hybrid value chains have turned out to be an indispensable source of competitiveness and growth. Below is a non-exhaustive list of companies that are running successfully theoretically irreconcilable strategies and benefitting from unconventional synergies. Players that are ignoring the new paradigm are doing so at their peril. They will miss out on numerous potential customers and sources of savings. There are too many opportunity costs to be stuck with one business model!

Fig. 1: Based on Porter’s competitive advantage, there are three main business models: volume, premium, low-cost. Four combinations of these business models can be found, with one of the combination covering the full range of possible strategies, as exemplified by Renault-Nissan (first automobile maker in the world) or Accor (6th largest hotel group in the world)

| Industry | Company | Low cost Brand | Mainstream brand | Premium brand | |

| Car rental | Hertz | Firefly | Hertz | ||

| Avis | Budget,

Thrifty, (Zip Car) |

Avis | |||

| Europcar | InterRent | Europcar | |||

| Air transport | SIA | Tiger Air

Scoot |

SilkAir | Singapore Airlines | |

| Lufthansa | Germanwings

Eurowings |

Lufthansa | |||

| IAG | Vueling | British Airways & Iberia | |||

| Hotels | Accor | Motel 6

Ibis Budget Formule 1 |

Novotel

Mercure |

Sofitel | |

| Pay TV | Sky TV | NOW TV | Sky TV | ||

| Silicon | Dow Corning | Xiameter | Dow Corning | ||

| Car | Nissan | Datsun | Nissan | Infiniti | |

| Renault | Dacia | Renault | Alpine | ||

| Toyota | Toyota | Lexus | |||

| Fiat | Fiat, Chrysler | Ferrari | |||

| Tyres | Michelin | Kormoran, Riken | Kleber | Michelin | |

| Railway | SNCF | Ouigo, Ouibus | TGV | ||

| Food retail | Casino | Leader Price | Geant Casino | Monoprix | |

| Telecom | Orange | Sosh | Orange | ||

| Eyewear | Afflelou | Optical Discount | Alain Afflelou | ||

| Insurance | Axa | Direct Assurance | Axa | ||

| Fitness centers | Moving | Fitness Park | Moving Express | Club Moving | |

Table 1: some industries where companies run simultaneously supposedly incompatible business models and combine supposedly incongruous competitive advantages