At a time when value comes from combination, too much focus means narrow-mindedness and lost ground. Firms have to go beyond their efficiency comfort zone to discover and exploit hidden synergies between supposedly competing business models.

For decades, the key word in organizations has been Focus. Superior financial performance would derive from focus on one’s competitive advantage, focus on one’s objectives, focus on one’s clients. In a turbulent world, this is no longer true. Too much focus prevents from seeing the big picture and the new offerings that are likely to attract core and remote clients. The excess of focus has become a strategic handicap, leaving incumbent firms in the uncomfortable position of running desperately after new entrants.

The new business imperative is Combine! Competitive advantages come nowadays from the association of elements that are usually treated in isolation and perceived as unrelated or incompatible. With hindsight, we realize how smart it was from Google to develop and offer for free what was considered at the time as a distraction. Thanks to this clairvoyance, Android has become the Trojan horse that guarantees Google’s omnipresence on mobile devices. Non technology-based firms can also rejuvenate their core business by looking for other ways of fulfilling their clients’ needs.

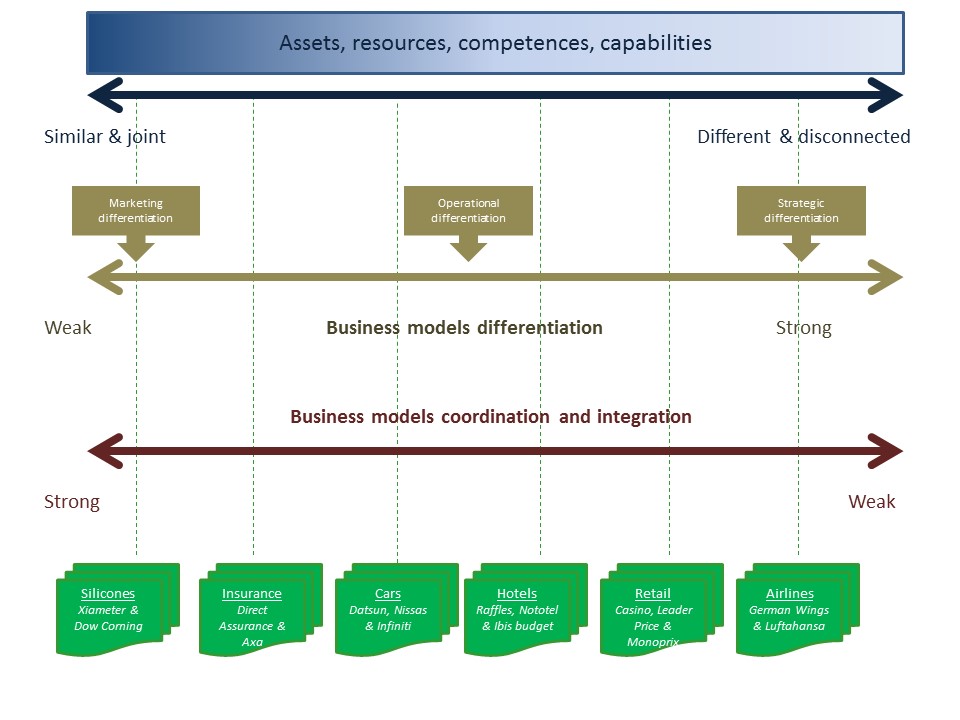

Increased organizational agility have changed the foregone conclusion that firms had to focus on one business model and execute it brilliantly. Designing the right value chain in a company with multiple business models boils down to finding the right balance between differentiation and integration. The challenge is to manage independently what has to be differentiated and integrate properly what has to be pooled, in order to ensure scale and cost advantages that cannot be matched by pure players. The ability to manage this complexity becomes an additional source of competitive advantage, difficult to decipher and imitate.

All activities that have no impact on clients’ perception and may generate scale economies are pooled, which usually include IT, procurement, back office support. Conversely, specific brands and marketing are necessary in order to create distinct identities and territories, and minimize cannibalization. Depending on the industry, a deeper and more operational differentiation will be required in addition to the marketing specialization. In the automotive industry, manufacturing will be specific to each business model but components, platforms, engineering competences, design, and distribution network will be shared.

These operational synergies are indispensable to reach a price level unmatchable by new entrants and achieve a good profitability. Dacia, which was originally a Romanian car builder, was bought out by Renault in 1999 and relaunched in 2004 as its “entry brand”. In ten years, the Dacia brand has sold 3.5 million vehicles (mostly in Europe and in the emerging countries). The Kwid was then designed as the brand’s seventh and ultra low-cost vehicle, to be manufactured in India. It is the fifth best-selling vehicle in India, six months after its launch in 2016, thanks to its unrivalled price of 3.900 $.

Fig 1: The Kwid

Industries can be positioned according to the number of obvious and hidden synergies that can be exploited (see fig. 2). At one end of the spectrum, integration is maximal and differentiation minimal. All activities are shared, except sales and marketing. Development and production activities are pooled as there are no real differences in the products themselves. For instance, in the silicones industry, Dow Corning Chemicals responded to low price competitors by offering its mainstream offer at a 20% discount in a dedicated entity Xiameter. Xiameter’s clients are price sensitive professionals who don’t mind ordering online, in bulk quantities with no client service at all. Similarly in the European insurance industry, where traditional companies acquired all pure Internet low cost players, activities of contract conception and production, risk assessment and management, administration and billing, claim handling were merged, leaving just marketing and customer service as specialized units.

Fig 2: Managing synergies between competing business models

As more progress is made towards the right end of the continuum, there are fewer obvious commonalities but greater potential to take the lead over focused players. In the hotel industry, core activities such as, online distribution, online marketing, IT systems (reservation system), purchasing of commodities (energy, telephony, laundry), real-estate management skills can fruitfully be leveraged to combine business models and multiply market approaches.